India Economy Iran War: Rupee at Record Low, Sensex Down 10% How Bad Can It Get?

The India economy Iran war equation is the most important domestic economic story of 2026 that most Indian media is covering inadequately fragmented into daily market updates and commodity price reports, without assembling the full picture of what a sustained Iran conflict does to India’s growth trajectory, its currency, its inflation rate, and the 330 million households whose energy costs are now directly linked to decisions made in Washington, Tehran, and Islamabad. The war began on February 28. It is now almost two months old. The Islamabad talks have failed twice. The ceasefire is holding nominally while the US naval blockade continues and IRGC gunboats fire on ships in the Indian Ocean. And India’s economy which was tracking toward 7% GDP growth heading into 2026 has absorbed shock after shock, with its central bank warning of inflation risks, its equity markets down sharply, its rupee at a record low, and its growth forecasts revised downward by every major international institution. This article assembles the full picture.

The Oil Channel: India’s Most Direct Exposure

India imports approximately 85% of its crude oil requirements. Before the Iran war, the price of Brent crude was around $72-75 per barrel well within a comfortable range for the Indian economy. The February 28 strikes and the subsequent Hormuz crisis pushed prices sharply higher. The current range is $80-85, reflecting a war premium on top of underlying supply-demand dynamics.

Every $10 increase in crude oil prices has a cascading effect through the Indian economy. The direct effect is on India’s import bill each $10 rise adds approximately $15 billion to India’s annual crude import cost, widening the current account deficit by roughly 0.4-0.5% of GDP. The indirect effect is broader: higher crude prices feed into diesel and petrol prices, which feed into transport costs, which feed into every consumer good in India. Economists estimate that a sustained $100 per barrel oil price could push India’s retail inflation CPI above 5%, with every 10% rise in crude prices adding 40-60 basis points to CPI.

The Gita Gopinath analysis from her April 23 interview with India Today TV is the clearest public statement of what the scenarios look like. If the Iran conflict is resolved in the next few days, the impact on India will be minimal. If oil prices average $100 per barrel, world growth falls from the current 3.1% projection to approximately 2.5%, and India as a country that relies heavily on the Middle East for energy and remittances faces a much more severe impact. If the war extends into May-June without resolution, the damage compounds significantly. The RBI has already built in a downside scenario to its April policy statement: it cut its April-June quarter growth forecast to 6.8% from 6.9%, and its July-September forecast to 6.7% from 7.0%.

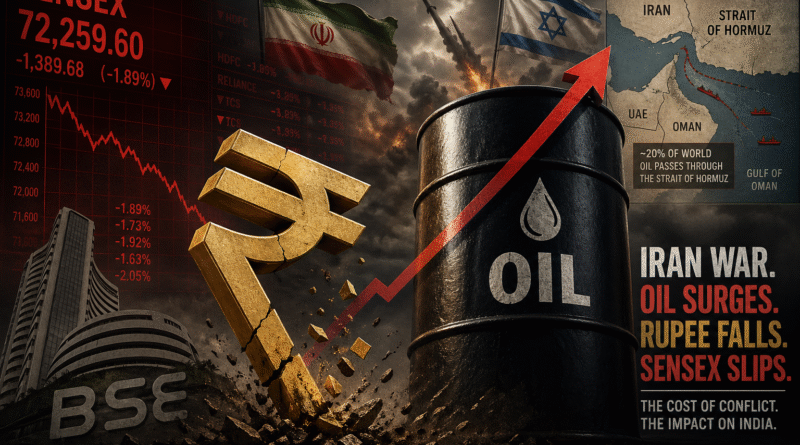

The Rupee: Why 93.94 Is Not Just a Number

The Indian rupee hit a record low of 93.94 against the US dollar in the weeks following the Iran war’s escalation. That number matters beyond the headline the rupee’s depreciation against the dollar is a direct amplifier of India’s oil import costs, since crude oil is priced in dollars globally. When the rupee weakens and oil prices rise simultaneously, the combined effect on India’s import bill is multiplicative, not additive.

A rupee at 93.94 versus the pre-war level of approximately 84-85 means every barrel of oil costs India roughly 10-11% more in rupee terms beyond the dollar price increase. This currency channel is particularly damaging because it is less visible to policymakers and the public than the headline oil price but its economic impact is equally real. Indian companies that import raw materials, machinery, or components priced in dollars face higher costs. Indian corporates with dollar-denominated debt face higher repayment burdens. And the RBI faces a dilemma: if it raises interest rates to defend the rupee, it risks slowing domestic demand and further reducing growth. If it lets the rupee fall, inflation accelerates.

The RBI’s decision to hold rates at 5.25% at its April meeting despite the rupee weakness and oil price surge reflects this dilemma. Governor Sanjay Malhotra’s statement was carefully worded: the intensity and duration of the conflict pose a “risk to inflation and growth.” That dual risk stagflation, where growth slows and inflation rises simultaneously is the scenario every Indian policymaker is trying to avoid. The RBI is essentially betting that the Iran war will be resolved before the stagflation risk materialises. If the Islamabad talks fail completely and the war extends another two months, that bet becomes very difficult to maintain.

The Stock Market: $12 Billion in Foreign Investor Outflows

The Sensex fell approximately 10% in the month following the February 28 escalation. That number understates the market’s anxiety: over 400 individual stocks faced sharp declines, and foreign institutional investors sold a net $12.14 billion worth of Indian shares as of mid-March 2026. That foreign investor outflow $12 billion in roughly six weeks is one of the largest sustained FII exits from Indian markets since the COVID-19 crash of March 2020.

The logic behind the foreign investor retreat is straightforward. India is an oil-importing emerging market with significant current account deficit sensitivity to energy prices. When oil rises and the rupee falls simultaneously, the dollar-denominated returns on Indian equity investments deteriorate even if the underlying Indian businesses are performing adequately. A foreign investor holding Indian equities loses in two ways simultaneously when oil spikes the stock prices fall in rupee terms, and those rupee returns are worth fewer dollars when converted back. The $12 billion outflow reflects rational risk management by institutional investors, not a fundamental reassessment of India’s long-term growth story.

Goldman Sachs and Moody’s have both revised India’s GDP growth downward to 5.9-6% in scenarios where oil sustains at $100 or above. These revisions, published in mid-March when the Hormuz crisis was at its peak, assumed the conflict would be prolonged. With the ceasefire nominally holding but the diplomatic process having failed twice, the Goldman-Moody’s scenario is closer to the base case than the IMF’s 6.5% optimistic forecast.

The Remittance Channel: 8 Million Indians in the Gulf

One of the most underanalysed dimensions of the India economy Iran war impact is the remittance channel. India has approximately 8 million workers in the Gulf UAE, Saudi Arabia, Kuwait, Qatar, Oman, Bahrain. Their combined annual remittances to India amount to over $50 billion making the Gulf the single largest source of India’s foreign remittances, which in aggregate are the largest source of foreign exchange inflows for the Indian economy, exceeding even FDI.

The Iran war threatens this remittance channel through two mechanisms. The first is direct: Iran fired missiles at UAE military installations hosting US forces, and the IRGC has been attacking ships in the Gulf of Oman. Gulf-based Indian workers face physical safety risks that, if they escalate into a broader Gulf conflict, would trigger emergency evacuations similar to Operation Kaveri (Sudan, 2023) or Vande Bharat Mission (COVID). The Indian government has no public plan for a Gulf worker evacuation at this scale — 8 million people from five different countries simultaneously and the logistical challenge would be staggering.

The second mechanism is economic: if the Iran war drives Gulf economies into recession through disrupted energy exports, reduced government revenues, and decreased construction and services activity Gulf employers reduce their workforces. Indian migrant workers, who often have limited formal labour protections, are typically the first to be laid off in a Gulf economic downturn. A reduction of even 10% in Gulf remittances would remove $5 billion from India’s annual foreign exchange inflows equivalent to erasing the benefit of the UK FTA in a single year.

The Jan Vishwas Offset: India’s Domestic Buffer

Not everything in the India economy Iran war picture is negative. India has a genuine domestic economic buffer that is limiting the damage from external shocks and it is worth acknowledging.

The Jan Vishwas (Amendment of Provisions) Bill 2026 passed in April 2026 decriminalised 784 provisions across 79 central Acts, converting criminal penalties for technical business errors into civil penalties. This is the largest single deregulation of India’s business environment since the GST reform of 2017. By removing the threat of imprisonment for procedural errors, India is reducing the compliance burden on MSMEs which navigate up to 1,450 annual regulatory requirements and signalling to foreign investors that India’s regulatory environment is converging with global standards.

The IMF’s baseline 6.5% growth forecast for India actually reflects two opposing forces: a negative shock from the Iran war and a positive shock from the tariff reduction under the India-US trade deal (from 50% to 10%) and the Ease of Doing Business improvements. As Gopinath noted explicitly, in India’s case these two forces “offset each other” which is why even the IMF’s downside scenarios have India growing faster than most major economies. India at 6% growth during a global oil shock is still outperforming every G7 economy and most of its Asian peers.

The RBI’s liquidity management has also been a stabilising force. Systemic liquidity has moved from a deficit of Rs 3.1 lakh crore in mid-January to a surplus of approximately Rs 1.5-2 lakh crore by early April, providing a buffer for domestic credit demand even as external headwinds intensified. India’s foreign exchange reserves, while under pressure from the rupee defence, remain above $680 billion sufficient to cover approximately 10 months of imports, well above the standard adequacy benchmark of 3 months.

What the Numbers Mean for Ordinary Indians

Behind every percentage point of GDP growth revision is a real-world impact that reaches ordinary Indian households. If India’s growth slows from 7% to 6%, the difference in absolute rupee terms is approximately Rs 2-2.5 lakh crore in annual GDP. That translates into fewer jobs created, lower wage growth, reduced government tax revenue, and less fiscal space for social spending on health, education, and infrastructure.

For the 80 million Indian households using LPG for cooking and the 250 million more using subsidised kerosene or firewood as alternatives the energy price impact of the Iran war is already visible. The LPG shortage of March 2026 forced the government to declare an energy emergency and implement emergency procurement at spot prices significantly above contracted rates. Every month the Hormuz disruption continues adds to that procurement cost, which either feeds through to higher consumer prices or is absorbed by the government as a fiscal subsidy burden that reduces spending elsewhere.

For the urban middle class, the Iran war is visible in fuel prices, food inflation (since every food item has a transport cost embedded in its price), and the portfolio losses from the Sensex decline. For rural India, it is visible in fertiliser prices India imports significant quantities of natural gas-derived fertiliser precursors through Gulf channels and in the cost of the diesel that powers irrigation pumps, tractors, and the trucks that move agricultural produce from farm to market.

ThirdPol’s Take

The India economy Iran war story has two distinct time horizons. In the short run — the next four to eight weeks India’s economic trajectory is almost entirely hostage to whether the Hormuz disruption resolves. If the Iran talks produce a deal in May, oil prices normalise, the rupee stabilises, and the Goldman-Moody’s downside scenarios become history rather than forecasts. If the talks fail again and the war extends into June-July, the RBI’s dilemma deepens, the $12 billion FII outflow becomes $20 billion, and the 6.5% IMF forecast becomes the ceiling rather than the base case. In the medium run the next two to three years the Iran war will actually have accelerated structural changes that are good for India: faster trade diversification away from single-market dependency, accelerated domestic energy investment, faster defence manufacturing indigenisation, and a sharper focus on reducing import dependency in energy-intensive sectors. India enters every crisis somewhat stronger because crises force the institutional adaptation that peacetime complacency defers. The current one is no different provided it does not last long enough to break the growth momentum that has been India’s most important geopolitical asset.

Amit Mangal writes on India’s foreign policy and geopolitics at ThirdPol. Follow ThirdPol on X and LinkedIn.